Adobe Vs. 메타 플랫폼 - 타이탄 충돌 시

Introduction소개

Recently, two articles emerged on Meta Platforms, Inc. (FB), each posing a unique statement or proposition.최근, 메타 플랫폼 주식회사(FB)에 각각 독특한 진술이나 제안을 하는 두 개의 기사가 등장했다.Fellow SA Contributor @ 믿고, 투자자들은 새로 생겨나는 웹 3.0 미래에 노출되길 원한다면 다른 곳을 보기 시작해야 한다. The metaverse may seem like a natural extension for Facebook, but I believe this expansion is outside of the company's core competencies. 메타버스(metaverse)는 페이스북의 자연스러운 확장처럼 보일지 모르지만, 나는 이 확장이 회사의 핵심 역량에 미치지 못한다고 믿는다.Meta Platforms Core Competencies메타 플랫폼 핵심 역량

Facebook was -type="disc">- Social Media Platforms (Facebook - 2.91 billion users, Instagram - 1.07 billion users, WhatsApp - 2.0 billion users, Facebook Messenger - 1.3 billion users, and Workplace - 7 million users as of May 2021) - 3.58 billion Family Monthly Active People as of FY 2021 Q3 Earnings Call 소셜 미디어 플랫폼(Facebook - 29억1000만 사용자, 인스타그램 - 10억7000만 사용자, 왓츠앱 - 20억 사용자, 페이스북 메신저 - 13억 사용자, Workplace - 700만 사용자 2021년 5월 현재) - 35억8000만 가족 월별 액티브 피플링 콜 2021년 3분기 기준

Source:

Source: Source: Source: 사용되는데, 이는 회사 수익의 약 97%를 차지하기 때문이다. Additional elements include improvements of algorithms for facial recognition and engagement. 추가적인 요소들로는 안면 인식과 관여를 위한 알고리즘의 개선이 포함된다. Facebook IQ may be the underlying basis for the computing platform envisioned by the company. 페이스북 IQ는 회사가 구상하는 컴퓨팅 플랫폼의 기초가 될 수 있다.

Source: 2 헤드셋 2021년 11월 현재 1,000만 대 출고), Virtual Reality 환경(Horizon Worlds), Facebook Reality Labs.

Source: Facebook Marketplace with Sans Light';">Source: Source: : 'Noto Sans Light';">Source: 투로 보았다. Not only are there

Source: Source: Source: 필자의 이전 기사에 근거하여 알고 있듯이, 나는 Meta Platforms가 (회사를 위한) 수많은 신규 시장으로의 과도한 인수합병에 대해 비관적이다.

Consider Adobe's leadership alone in each segment.각 부문에서 Adobe의 리더십만 고려하십시오. The company sets the TAM for each market and has an incredibly in-depth understanding of the customer audiences and customer segments, and how to reach each one, invite them into Adobe's expansive ecosystem, build goodwill, and monetize it. 이 회사는 각 시장에 대한 TAM을 설정하고, 고객 청중과 고객 부문에 대한 이해와 각 고객에 대한 접근법, Adobe의 확장된 생태계에 그들을 초대하고, 친선을 구축하며, 그것을 수익화하는 방법을 믿을 수 없을 만큼 깊이 있게 이해하고 있다. For evidence of the above, look no further than the Source: Source: , 협업, 통신 및 전자서명[계약 또는 감사용]과 같은 비즈니스 기능을 위한 고품질 소프트웨어의 확산은 Adobe가 상인 및 비즈니스와의 디지털 경제에서 메타 플랫폼 자체의 노력에 대항하여 엔터프라이즈 공간 내에서 활용할 수 있는 고유한 이점을 나타낸다.es. This is an offering entirely lacking from Meta Platforms' own ecosystem and product portfolio.es. 이것은 메타 플랫폼의 자체 에코시스템과 제품 포트폴리오에서 완전히 부족한 제품이다.

Source: 중요한 것은, Adobe는 Meta Platforms가 소셜 미디어 오퍼링에 도입하고자 하는 모든 새로운 영역에 확립된 생태계를 가지고 있다는 점이다.Here is Adobe's leadership position in the "creator economy:""창조경제"에서 Adobe의 리더십 위치는 다음과 같다.

Source: Source:

Source: Source: , 알테릭스, 오라클, 세일즈포스, IBM 등 수많은 경쟁업체들이 존재한다는 것을 다시 한 번 명심하면서 전자상거래에 적합한 "컴퓨터 플랫폼"으로서의 성공과 연계되어 있다.

Source: Source: Source: )에 대항하는 "창조경제", "전자상거래" 그리고 "컴퓨팅 플랫폼"의 시장에서 극심한 저항에 직면할 것이라고 믿는지를 정확히 이해하고 싶다.

Meta Platforms (Facebook) Advantages메타 플랫폼(Facebook)의 이점

Meta Platforms (Facebook) has the following advantages:메타 플랫폼(Facebook)에는 다음과 같은 장점이 있다.1. Adobe has $3.1. Adobe는 3달러를 가지고 있다.8B in cash and cash equivalents, $8.7B in Total Current Assets, and $27.2B in Total Assets as of 3-Dec-2021.현금및현금성자산으로 8B, 총유동자산으로 8.7B, 총자산으로 27.2B 달러 3-12-2021년 현재. Meta Platforms has $14.5B in cash and cash equivalents, $75.4B in Total Current Assets and $170B in Total Assets as of 30-Sep-2021. 메타 플랫폼은 현금 및 현금성 자산이 14.5B 달러, 총 유동 자산이 75.4B 달러, 총 자산이 170B 달러(30-Sep-2021년 기준)이다.This is 3.8x for cash and cash equivalents, 1.7x for Total Current Assets, and a whopping 6.3x for Total Assets.이는 현금및현금성자산의 경우 3.8배, 총유동자산의 경우 1.7배, 총자산의 경우 무려 6.3배이다. For Adobe, Goodwill accounts for $12.7B (47% of Total Assets) while for Meta Platforms Goodwill accounts for only $19.1B (11% of Total Assets). Adobe의 경우 영업권은 12.7B 달러(총 자산의 47%)를 차지하며, 메타 플랫폼의 영업권은 19.1B 달러(총 자산의 11%)에 불과하다.Adobe sports $4.67B in total debt while Meta Platforms has $13.어도비 스포츠는 총 부채 $4.67B인 반면 메타 플랫폼은 $13이다.2B in total debt, based on Seeking Alpha.총 부채 2B, '알파 찾기' 기준Thus, we can immediately conclude that Meta Platforms, at first look, has a fortress-like balance sheet that it can rely upon.따라서, 우리는 메타 플랫폼이 처음에는 믿을 수 있는 요새 같은 대차대조표를 가지고 있다고 즉시 결론을 내릴 수 있다.2. Meta Platforms owns the largest social media platforms in the world, giving it scale to influence countless (3 billion+) individual consumers and businesses all at once.2. 메타 플랫폼은 세계에서 가장 큰 소셜 미디어 플랫폼을 소유하고 있어, 수많은 (30억 이상) 개별 소비자와 기업에 한꺼번에 영향을 미칠 수 있는 규모를 제공한다. If the company leverages its network, only 10% of users would translate into 300 million potential customers for the two of the new projects (creator economy and e-commerce). 회사가 네트워크를 활용한다면 신규 프로젝트 두 개(창조경제와 전자상거래)에 3억 명의 잠재 고객으로 전환되는 사용자는 10%에 불과하다.

/>

Source: 있기 때문에 이 회사가 차별화된 이점을 제공한다. It remains unclear, however, if this will play a key differentiating role in competing against Adobe in the creator economy, e-commerce, and compute platform markets, as we will discuss later. 그러나 이것이 나중에 논의할 것처럼 창조경제, 전자상거래, 컴퓨팅 플랫폼 시장에서 Adobe와 경쟁하는 데 핵심적인 차별화 역할을 할지는 여전히 불확실하다.

Adobe Advantages어도비 장점

Adobe, in turn, has the following advantages:결과적으로 Adobe는 다음과 같은 이점을 가지고 있다.1. While Meta Platforms faces nearly weekly 인수와 같은 다양한 프로젝트에 대해 규제당국의 지속적인 차단에 직면해 있다.Adobe, in the meantime, is a smaller and more agile firm that can easily acquire other start-ups or companies via tuck-in acquisitions (such as firms. 규제 당국은 PDF를 사용하여 다른 S&P 500 기술 기업을 비판하고 협력한다.

Source: it and to convince customers to utilize new product offerings. 따라서 메타 플랫폼의 장점 #2는 일단 신뢰가 상실되면 그것을 되찾고 새로운 제품 오퍼링을 활용하도록 고객에게 설득하는 것이 종종 엄청나게 어려운 것처럼 보인다.3. While Meta Platforms faces an exodus of 생태계, 제품, 공공의 약속은 '누구나 창조자가 될 수 있다'는 포괄적 문화를, 메타 플랫폼의 혐오 발언, 정치, 오보, 데이터 침해, 폭력 스캔들은 분열의 문화를 그린다. While it's true that Meta Platforms' social media platforms can be used to connect and to communicate with friends and family, that "connection" comes at increasing risk of reading or witnessing something unpleasant and charged. 메타 플랫폼의 소셜 미디어 플랫폼을 친구 및 가족과 연결하고 소통하는 데 사용할 수 있는 것은 사실이지만, 그러한 "연결"은 불쾌하고 유료화된 내용을 읽거나 목격할 위험이 커진다.4. Adobe has existing, highly-functional, and effective differentiator products in its Document Cloud, Creator Cloud, and Experience Cloud business franchises, which in essence translates into a first-mover advantage for Adobe.4. Adobe는 Document Cloud, Creator Cloud, Experience Cloud 비즈니스 프랜차이즈에 기존 고기능의 효과적인 차별화 요소 제품을 보유하고 있으며, 이는 본질적으로 Adobe에게 있어 퍼스트 무버 우위로 해석된다. If Meta Platforms chooses to compete in these spaces (as the intention suggests via the FY Q2 2021 earnings call), Adobe's dominance with respect to the software offerings and understanding of customer trends give it an immediate competitive edge. (FY 2분기 2021 어닝 콜을 통해 의도한 대로) 메타 플랫폼이 이러한 공간에서 경쟁하기로 선택한 경우, 소프트웨어 제품 및 고객 동향에 대한 이해에 관한 Adobe의 지배력은 즉각적인 경쟁 우위를 제공한다. Adobe's vision, prominence, and proven reliability give consumers trust that Adobe is reputable and sincere in its promise of "Creativity is for Everyone." 어도비의 비전과 탁월함, 그리고 입증된 신뢰성은 소비자들에게 "창의성은 모두를 위한 것이다"라는 약속에서 어도비가 명성이 자자하고 성실하다는 믿음을 준다.

Source: 할 것이다. This takes time, resources, effort, and concentration. 이것은 시간, 자원, 노력, 집중을 필요로 한다.5. Some investors believe that Meta Platforms' (Facebook's) switching costs are very high and that they do not foresee other companies disrupting the social networks or effectively stealing users.5. 일부 투자자는 '메타플랫폼'(페이스북)의 전환 비용이 매우 높고, 다른 기업이 소셜 네트워크를 교란하거나 효과적으로 사용자를 도용할 것으로 예상하지 않는다고 생각한다. While it's true that Meta Platforms' social media platforms have some degree of switching costs, I believe Adobe's strategy and switching costs are far more effective and stickier. 메타 플랫폼의 소셜 미디어 플랫폼이 어느 정도 스위칭 비용이 드는 것은 사실이지만, 어도비의 전략과 스위칭 비용이 훨씬 더 효과적이고 고착적이라고 생각한다. Here is why: 그 이유는 다음과 같다.

Meta's Switching Costs:메타 전환 비용:

The primary reasons quoted for the switching costs associated with Meta Platforms are a) customers ability to connect, to communicate, and to share experiences and memories with friends and family, usually via digital formats such as pictures, videos, and the written word; b) small businesses' and merchants' dependence on marketing and advertising 메타 플랫폼과 관련된 전환 비용에 대해 인용되는 주요 이유는 a) 일반적으로 사진, 비디오 및 글자와 같은 디지털 형식을 통해 고객과의 연결, 커뮤니케이션 및 경험 및 추억을 친구와 가족과 공유할 수 있는 능력, b) 중소기업 및 상인들의 마케팅 및 광고 의존성이다. via Facebook for their livelihoods; c) the network effect - there are so many users that it doesn't make sense to switch away to a less dominant platform.생계를 위해 페이스북을 통해; c) 네트워크 효과 - 사용자가 너무 많아서 덜 지배적인 플랫폼으로 전환하는 것은 말이 되지 않는다.Yet Meta Platforms' brand and image issues directly counteract much of the advantage brought on by the design of its ecosystem, network effect, and products.그러나 메타 플랫폼의 브랜드와 이미지 이슈는 그것의 생태계, 네트워크 효과, 그리고 제품들의 설계에 의해 야기되는 많은 이점에 직접적으로 대항한다. Customers, if disgruntled enough, can absolutely pursue any number of other social media offerings and downloading one's pictures, videos, and portions of the written / posted content is not as difficult as some claim. 고객들은, 충분히 불만족스럽다면, 절대적으로 많은 다른 소셜 미디어 제공물을 추구할 수 있고, 누군가의 사진, 비디오, 그리고 쓰여진/게시된 콘텐츠의 일부를 다운로드 받는 것은 몇몇 사람들이 주장하는 것만큼 어렵지 않다. Small businesses and merchants may be becoming increasingly worried about the association with Meta Platforms (Facebook) because the company is losing trust with consumers, regulators, and even businesses. 중소기업과 상인들은 메타플랫폼(Facebook)과의 연관성에 대해 점점 더 걱정하게 될 수도 있는데, 왜냐하면 이 회사는 소비자, 규제당국, 그리고 심지어 기업과의 신뢰를 잃고 있기 때문이다. The network effect and the social media platforms themselves, built on what many now believe to be an inherently flawed and misused business model, are ripe for disruption. 네트워크 효과와 소셜 미디어 플랫폼 그 자체는 많은 사람들이 본질적으로 결함이 있고 잘못 사용된 비즈니스 모델이라고 믿는 것에 기초하여 구축되었으며, 붕괴될 가능성이 무르익었다.

Source: design that do not force users to scroll through countless advertisements; b) building goodwill with users via the free product offerings and converting users to priced tiers (with additional features) once a user understands the prod설계상 Adobe는 a) 사용자가 수많은 광고를 스크롤하도록 강요하지 않는 창의성과 디자인을 위해 고품질의 무료 제품을 제공하는 것, b) 무료 제품 오퍼링을 통해 사용자와 친선 관계를 구축하고 사용자가 prod를 이해하면 (추가 기능이 있는) 가격 계층으로 사용자를 변환하는 것 등과 같은 몇 가지 고유한 이점을 가지고 있다.uct and enjoys it [the recently launched Creative Cloud Express is a brilliant example of this strategy]; c) allowing businesses, merchants, creators and even non-professionals to utilize Adobe's amazing Hollywood grade products for creativity (video, drawing, illustration, editing, audio, etc.) without fear of repercussion from polarized content ouct와 그것을 즐기고[최근 출시된 Creative Cloud Express는 이 전략의 훌륭한 예다]; c) 기업, 상인, 크리에이터, 심지어 비전문가들도 양극화된 콘텐츠로 인한 반향을 두려워하지 않고 Adobe의 놀라운 할리우드 등급 제품을 창의성(비디오, 그림, 일러스트, 편집, 오디오 등)에 활용할 수 있도록 허용. or negative publicity (or at least with this being a rare case-specific exception).부정적 홍보(또는 최소한 이것이 드문 사례별 예외인 경우) Adobe has strong customer engagement and retention as a result. 결과적으로 Adobe는 강력한 고객 참여와 보존을 가지고 있다.

6. Meta Platforms is distracted with 어떤 것이든 성공하기를 바라는 절박한 희망 속에서 수많은 프로젝트와 베팅을 한꺼번에 과다하게 할 작정인 것 같다.The company is struggling to hold its own against other social media platforms, in essence being forced to acquire competitors or to replicate competitors' features in recent years to stay relevant, yet it seemingly believes competing with even more firms is a wise strategy.그 회사는 다른 소셜 미디어 플랫폼에 대항하기 위해, 본질적으로 경쟁자를 획득하거나 관련성을 유지하기 위해 최근 몇 년 동안 경쟁자의 특징을 복제하도록 강요당하면서, 다른 소셜 미디어 플랫폼에 대항하기 위해 고군분투하고 있지만, 훨씬 더 많은 회사와 경쟁하는 것이 현명한 전략이라고 믿고 있다. TikTok, for example, is rumored to have, 앱 추적 투명성(Apple의 iOS 14 변경에 대응한 표적 광고 개선 / ATT, 유럽의 디지털 서비스법 시행 전), 젊은 사용자의 보유, e-com과 같은 중요한 주제에 14" />

Meta Platforms' Balance Sheet (Advantage #1) will not be an effective competitive advantage or edge against Adobe (and countless other firms) as it overdiversifies and tries to compete in more industries and markets while flailing in its core businesses (social media platforms).메타 플랫폼의 대차대조표(어드밴티지 #1)는 어도비(및 수많은 다른 기업)가 자사의 핵심 사업(소셜 미디어 플랫폼)에서 허우적거리며 더 많은 산업과 시장에서 경쟁하려고 하기 때문에 어도비(그리고 수많은 다른 기업)에 대한 효과적인 경쟁우위나 우위가 되지 않을 것이다.Adobe, in the meantime, is organized, swift, and beating the competition.그 사이에 Adobe는 조직적이고, 빠르고, 경쟁에서 이긴다. A key example is the 이미지, 셔터스톡, 코렐 코퍼레이션, 에이비드, 쿼크 소프트웨어에 대해 뚜렷한 우위를 점하고 있다. In its Creative Cloud offerings, Adobe's ecosystem continues to act as a firm competitive advantage over standalone product offerings. 크리에이티브 클라우드 제품에서 Adobe의 에코시스템은 독립형 제품 제품보다 확고한 경쟁 우위로서 계속 작용하고 있다.Even more importantly, Adobe's dominance and success comes frequently from organic and homegrown solutions, while Meta Platforms seems increasingly dependent on an acquisition strategy, which is being actively challenged by regulators.더욱 중요한 것은, Adobe의 지배력과 성공은 유기농 솔루션과 자체 개발 솔루션에서 빈번히 발생하는 반면, Meta Platforms는 규제당국의 적극적인 도전을 받고 있는 인수 전략에 점점 더 의존하고 있는 것으로 보인다.

Adobe - Disruption of Social MediaAdobe - 소셜 미디어 중단

If Meta Platforms wants to compete with Adobe, it's only fair to warn them that Adobe will be competing with Meta Platforms.메타 플랫폼이 Adobe와 경쟁하기를 원한다면 Adobe가 Meta 플랫폼과 경쟁할 것이라고 경고하는 것이 타당하다.Adobe is like the artistic genius with sinewy muscles concealed by elegant and perhaps overly eccentric clothing that misleads the bulky self-assured entrepreneur into believing that the fight will be an easy one.어도비는 우아하고 어쩌면 지나치게 괴팍한 복장으로 가려진 근육질의 예술적 천재와 같다. 이것은 덩치가 큰 자신감 넘치는 기업가를 오도하여 싸움이 쉬운 싸움이 될 것이라고 믿게 만든다.The issue with many traditional social media platforms is by now well known:많은 전통적인 소셜 미디어 플랫폼의 문제는 현재 잘 알려져 있다.

- The platforms targeted communication and connection of users first, quickly building up a critical mass and a network.플랫폼은 우선 사용자의 통신과 연결을 목표로 하여, 신속하게 임계 질량과 네트워크를 구축하였다. Growth in user numbers was prioritized over visualization and strategic thinking about the eventual business model or impact on humanity. 사용자 수의 증가는 궁극적인 비즈니스 모델이나 인류에 미치는 영향에 대한 시각화와 전략적 생각보다 우선시되었다.

- The platforms collected massive troves of user data in exchange for "free" social media products.이 플랫폼들은 "무료" 소셜 미디어 제품과 교환하는 대량의 사용자 데이터를 수집했다.

- The platforms began advertising insistently and selling user data, often without your permission.플랫폼은 종종 당신의 허락 없이 끈질기게 광고를 하고 사용자 데이터를 팔기 시작했다.

- To further boost and retain profits, certain platforms began to dramatize content on the platform to keep users engaged and glued to the screen as engagement drove better results.수익을 더욱 높이고 유지하기 위해, 특정 플랫폼은 참여가 더 나은 결과를 가져오자 사용자들의 참여와 화면 밀착을 유지하기 위해 플랫폼의 컨텐츠를 극화하기 시작했다.

- People didn't feel so well.사람들은 기분이 별로 좋지 않았다.

Adobe has a fledging social media platform (acquired in 2012) called Behance's business model is focused on giving human beings a higher calling - namely that of art and collaboration on creative value-add projects.1. Behance의 사업 모델은 인간에게 더 높은 소명, 즉 예술과 창조적 부가가치 프로젝트에 대한 협업의 소명을 부여하는 데 초점을 맞추고 있다. The platform focuses on displaying and having human beings collaborate on an endless flurry of magical, gorgeous, and inspiring digital works of art, while giving them the opportunity to connect and to communicate. 이 플랫폼은 인간이 서로 연결되고 소통할 수 있는 기회를 주는 동시에 마술적이고 화려하며 영감을 주는 디지털 예술 작품들을 끝없이 펼쳐놓고 협업하게 하는 데 초점을 맞추고 있다.

Source: Source: 위반하는 대신 소셜 미디어 플랫폼을 지속적으로 확장하기 위해 고품질 제품 오퍼링을 설계하고 유지할 수 있는 인센티브를 제공한다.r privacy, or spam you with advertisements.사생활을 보호하거나, 광고로 스팸을 참조하십시오.

Source: the investment case for one company over the other requires pairing both qualitative and quantitative elements.메타버스(Metavers)와 웹 3.0(Web 3.0)의 주제로 넘어가기 전에, 한 회사가 다른 회사보다 더 많이 투자하기 위해서는 질적 요소와 양적 요소를 모두 결합해야 하기 때문에 각 회사의 재무 실적과 관련 지표를 간략히 강조하고 싶다. We will use a simple scoring rating. 우리는 간단한 채점 등급을 사용할 것이다.Over the past 5 years, Adobe returns sit at 428.4% versus Meta Platforms (Facebook's) returns of 180.75%.지난 5년간 Adobe의 수익률은 428.4%로 Meta Platforms(Facebook의 수익률)의 180.75%를 기록했다. [+1 Adobe] [+1 Adobe]

Over the past 5 years, Facebook grew revenues by 306% versus Adobe's revenue growth of 157%.페이스북은 지난 5년 동안 어도비의 157% 매출 증가율과 비교해 306%의 수익을 올렸다. [+1 Meta Platforms] [+1 메타 플랫폼]

Yet the two companies are very close on Net Income growth, 267% for Adobe versus 294% for Facebook for the 5-year period.그러나 두 회사는 5년 동안 어도비 267%와 페이스북 294%로 순이익 증가에 매우 근접해 있다. [+1 Adobe / +1 Meta Platforms] [+1 Adobe / +1 메타 플랫폼]

Adobe's market capitalization sits at $262B versus Facebook's at $905B.어도비의 시가총액은 262B달러, 페이스북은 905B달러다. Adobe employs 22,516 employees versus ~x3 as much for Facebook, which employs 68,177 employees. 어도비는 직원 수가 2만2516명인 반면 페이스북은 6만8177명을 고용하고 있다. [+1 Adobe / +1 Meta Platforms] [+1 Adobe / +1 메타 플랫폼]Adobe has a gross profit margin of 88.18% versus Facebook's of 80.58%.어도비는 페이스북의 80.58%에 비해 88.18%의 매출총이익률을 기록하고 있다. Net income margin sits in favor of Facebook at 35.88% versus Adobe's at 30.55%. 순이익 마진은 페이스북이 35.88%로 어도비아가 30.55%보다 유리하다. Adobe's RoE and RoA sit at 34.37% and 14.08% versus Facebook's at 32.10% and 18.57%. 어도비의 RoE와 RoA는 페이스북의 32.10%, 18.57%에 비해 34.37%, 14.08%에 머물렀다. Levered FCF margin is 36.92% for Adobe versus 23.56% for Facebook. Leverber FCF 마진은 Adobe의 경우 36.92%, Facebook의 경우 23.56%로 나타났다. [+3 Adobe / +2 Meta Platforms] [+3 Adobe / +2 메타 플랫폼]Valuation, as least on a P/E basis, sits in favor of Facebook at TTM GAAP P/E of 23.92 versus Adobe's TTM GAAP P/E of 55.64.최소한 P/E 기준으로 평가하면 TTM GAAP P/E 23.92에서 Facebook의 손을 들어주고 Adobe의 TTM GAAP P/E 55.64를 지지한다. However, I believe DCF and EPS Valuation models are more effective in considering each company's undervaluation for comparative purposes. 다만 DCF와 EPS 밸류에이션 모델은 비교목적으로 각 기업의 저평가 방식을 고려할 때 더 효과적이라고 본다. [+1 Meta Platforms] [+1 메타 플랫폼]Many investors are dumbfounded and amazed by Meta Platforms perceived financial resilience and leverage with respect to R&D, OpEx, and CapEX, yet the company stacks up unfavorably against Adobe on both R&D and CapEX.많은 투자자들은 Meta Platforms가 R&D, OpEX, CapEX와 관련하여 재정적 복원력과 지렛대를 인식한 것에 대해 어안이 벙벙하고 놀라워하고 있지만 회사는 연구개발과 자본EX 모두에서 Adobe에 불리한 입장에 서 있다.Using TTM figures, Meta Platforms has R&D spend of $22.8B (20.3% of Total Revenues), Selling, General and Administrative spend of $22.1B (18.8% of Total Revenues), and Total Operating Expense of $46.9B (41.8% of Total Revenues).TTM 수치를 활용하면 메타플랫폼은 연구개발비 22.8B달러(총수익의 20.3%)와 판매비, 일반비 및 행정비 22.1B달러(총수익의 18.8%), 총운영비 46.9B달러(총수익의 41.8%)가 소요된다. Meta Platforms has Capital Expenditures of $17.8B, or 15.9% of Total Revenues. 메타 플랫폼은 총 수익의 15.9%인 17.8B 달러의 자본 지출이 있다. One should keep in mind both R&D and CapEx are expected to increase for Meta Platforms substantially in coming years. 향후 몇 년 안에 메타 플랫폼의 연구개발과 설비투자 모두 크게 증가할 것이라는 점을 명심해야 한다.Adobe has R&D spend of $2.5B (15.8% of Total Revenues), Selling, General, and Administrative (adding in Other Operating Expenses) of $5.6B (35.4% of Total Revenues), and Total Operating Expense of $8.1B (51.3% of Total Revenues).Adobe는 연구개발비용이 2.5B달러(총수입의 15.8%), 판매, 일반 및 관리비(기타영업비 추가)가 5.6B달러(총수익의 35.4%), 총운영비용이 8.1B달러(총수익의 51.3%)이다. Adobe has Capital Expenditures of $0.3B, or only an abysmally low 2% of Total Revenues. Adobe는 자본 지출이 0.3억 달러, 즉 총 수익의 2%에 불과한 형편없는 수준이다. [+2 Meta Platforms / +2 Adobe] [+2 메타 플랫폼 / +2 Adobe]On a comparative metrics tally, Adobe yields 8 versus Meta Platforms' 8.비교 메트릭스 집계에 따르면, Adobe는 메타 플랫폼의 8과 비교하여 8을 산출한다. If we add in Meta Platforms' fortress-like balance sheet (on a comparative basis), then the tally may be adjusted to 8 for Adobe versus 9 for Meta Platforms. 우리가 메타 플랫폼의 포트리스와 같은 대차대조표(비교 기준)를 추가한다면, 집계는 Adobe의 경우 8로, Meta 플랫폼의 경우 9로 조정될 수 있다.

Growth Prospects성장 전망

Modeling Meta Platforms' transition to the Metaverse looks something akin to the following, based on assumptions (covered in detail in a prior Source: Author's Calculations출처: 작성자의 계산Meta Platforms' future 10-year revenue growth is projected at ~22.35%.메타 플랫폼의 향후 10년 매출 성장률은 22.35%로 예측된다. The future EPS 10-year growth rate and FCF 10-year growth rate is projected at ~21.68% and ~24.93%, respectively. 향후 EPS 10년 성장률과 FCF 10년 성장률은 각각 ~21.68%, ~24.93%로 전망되고 있다. These rates are incorporated in valuation models. 이 요율은 평가 모델에 통합되어 있다. They are, of course, directional and not exact. 그들은 물론 방향성이 있고 정확하지 않다.Modeling Adobe's next 10 years' in turn requires an understanding of the latest commitments by leadership:Adobe의 향후 10년을 모델링하려면 리더십의 최신 약속을 이해해야 한다.

Source: Source: Source: 바탕으로 몇 가지 합리적인 가정을 할 수 있다.Adobe grew revenues by 16.2%, 22.9%, 21.9% and 23.7% during the 10Y, 5Y, 3Y, and TTM periods, respectively.어도비는 10년, 5년, 3년, TTM 기간 동안 각각 16.2%, 22.9%, 21.9%, 23.7%의 수익을 올렸다. Revenues for FY 2022 can be assumed at $17.9B as per the guidance. 2022 회계연도의 수익은 지침대로 17.9B 달러로 가정할 수 있다. Growth is being prioritized over operating margins, and Adobe's CEO is suggesting investors should expect accelerating growth despite only 13.4% expected revenue growth YoY in FY 2022. 영업이익보다 성장이 우선시되고 있으며, 어도비 CEO는 2022 회계연도의 YoY 예상 매출 증가율이 13.4%에 불과함에도 불구하고 투자자들은 빠른 성장을 기대해야 한다고 제안하고 있다. Margin expansion would likely follow more aggressively near the end of the 10-year period, and this is modeled accordingly. 마진 확장은 10년 기간이 끝날 무렵에 더욱 공격적으로 뒤따를 것으로 보이며, 그에 따라 모델링된다.

Source: Author's Calculations출처: 작성자의 계산Adobe's future 10-year revenue growth is projected at ~21.14%.Adobe의 향후 10년 매출 증가는 약 21.14%로 예상된다. The future EPS 10-year growth rate and FCF 10-year growth rate is projected at ~23.21% and ~18.58%, respectively. 향후 EPS 10년 성장률과 FCF 10년 성장률은 각각 ~23.21%, ~18.58%로 전망되고 있다. These rates are incorporated in valuation models. 이 요율은 평가 모델에 통합되어 있다. The growth rates are directional and not exact. 성장률은 방향성이 있고 정확하지 않다.

EPS Valuation and Discounted Cash Flow ModelsEPS 가치평가 및 현금흐름 할인모형

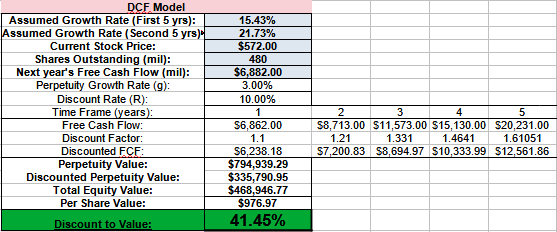

One can view the EPS and DCF Valuation Models below for both Meta Platforms and Adobe predicated on the assumptions modeled above for 10-year future growth rates, inclusive of EPS and free-cash-flow.EPS 및 자유현금 흐름을 포함하여 10년 미래 성장률을 위해 위에서 모델링한 가정에 근거한 메타 플랫폼과 Adobe 모두에 대한 아래의 EPS 및 DCF 평가 모델을 볼 수 있다. The DCF models do run to a full 10-year period; they are truncated for ease of readability. DCF 모델은 전체 10년 기간까지 실행된다. 읽기 쉽도록 잘린다.

Meta Platforms Valuation Models메타 플랫폼 평가 모델

Source: Author's Own Computations출처: 작성자 자신의 계산

Adobe Valuation ModelsAdobe Valuation Models

Source: Author's Own Computations출처: 작성자 자신의 계산Both companies appear undervalued based on EPS and DCF Valuation models, yet one belies a weakening of competitive advantages and increasing uncertainty regarding future business prospects, while the other is executing to long-term targets within the realm of its core competencies.두 회사 모두 EPS와 DCF 밸류에이션 모델에 기초해 저평가된 것처럼 보이지만 하나는 경쟁 우위의 약화와 미래 사업 전망에 대한 불확실성의 증가를 믿으며, 다른 하나는 핵심 역량의 영역 내에서 장기 목표를 달성하고 있다.The reasoning for this comes from a variety of fundamental factors that constitute each company's business model:이에 대한 추론은 각 기업의 비즈니스 모델을 구성하는 다양한 기본 요소에서 비롯된다.

- Meta Platforms is dependent on ~97% of its revenues from advertising from the legacy social media platforms - any materializing risk can quickly adversely impact profitability.메타 플랫폼은 기존 소셜 미디어 플랫폼의 광고 수익의 약 97%에 의존하고 있다. 즉, 실현되는 리스크는 수익성에 빠르게 악영향을 미칠 수 있다. Advertising revenue can be cyclical. 광고 수익은 순환적일 수 있다.

- Meta Platforms has committed to substantial R&D and CAPEX/OPEX investments in the coming 1-10 years to build out the Metaverse.메타 플랫폼은 메타버스 구축을 위해 향후 1~10년 동안 상당한 R&D 및 자본비용/OPEX 투자를 약속했다.

- Meta Platforms has committed to substantial R&D and CAPEX/OPEX investments in the coming 1-5 years to compete in the creator economy, e-commerce, and computing platforms.메타 플랫폼은 향후 1~5년 동안 크리에이터 경제, 전자상거래, 컴퓨팅 플랫폼에서 경쟁하기 위해 상당한 R&D 및 자본비용/OPEX 투자를 약속했다.

- Meta Platforms carries much greater risk of regulatory threats and lawsuits impacting the company's business model and profitability.메타 플랫폼은 회사의 비즈니스 모델과 수익성에 영향을 미치는 규제 위협과 소송의 위험이 훨씬 더 크다.

- Adobe's revenues are very well diversified between hundreds of customers and 3 core business franchises; Document Cloud, Creative Cloud, and Experience Cloud.Adobe의 매출은 수백 명의 고객과 3개의 핵심 비즈니스 프랜차이즈인 Document Cloud, Creative Cloud, Experience Cloud 사이에서 매우 다양하다.

- Adobe's revenues constitute high confidence of predictability as Adobe functions as a SaaS business model with high and growing ARR for each business segment.Adobe의 수익은 Adobe가 각 사업부문에 대해 높고 성장하는 ARR을 가진 SaaS 비즈니스 모델로서 기능하기 때문에 예측가능성에 대한 높은 신뢰도를 구성한다. This includes Remaining Performance Obligations. 여기에는 나머지 수행의무가 포함된다.

Source: Source: vast majority of profits (from advertisements) and the relegated relevance they will now have in the coming years.메타 플랫폼의 전략의 부조화는 회사의 새로운 유일한 초점인 메타버스(Metavers)와 (광고로부터) 막대한 이익을 창출하는 전통적인 소셜 미디어 플랫폼과 향후 몇 년 동안 그들이 갖게 될 관련성 강등 사이에서 겉으로 드러나는 단절감에서 비롯된다. One gets an immediate impression that these core competencies will be dismissed in favor of virtual and augmented reality headsets and environments, such as Horizon Worlds. 이러한 핵심 역량은 가상 및 증강현실 헤드셋과 Horizon Worlds와 같은 환경을 위해 폐기될 것이라는 즉각적인 인상을 받는다.

Canada" />

Source: , they have much catching up to do and such projects will be multi-year efforts (a favored phrase of late on Meta Platforms' earnings calls). 회사 자체 인정에 따르면, 그들은 할 일이 많고 그러한 프로젝트는 다년간의 노력(메타 플랫폼의 수익 전화에 대해 최근 호의적인 문구)이 될 것이다. Studio" />

Source: Source: 유명하다.The ultimate vision is to use these core competencies and markets as building blocks for the Metaverse, or the Web 3.0, as they will be integral in the future to a successful Metaverse / Web 3.0 platform and environment.궁극적인 비전은 이러한 핵심 역량과 시장을 메타버스(Metavers) 또는 웹 3.0(Web 3.0) 플랫폼과 환경을 성공적으로 구현하기 위해 향후 필수적으로 사용될 것이기 때문에 메타버스(Metavers) 또는 웹 3.0(Web 3.0)의 빌딩 블록으로 사용하는 것이다.Yet aside from the catch-up Meta Platforms needs to do to match the quality of Adobe's software offerings, there is one more immediate and troubling issue (aside from the privacy scandals, brand deterioration, regulatory risks, and expensive multi-year investments needed): there seems to be something inherently broken with the company's understandi그러나 Adobe의 소프트웨어 제품의 품질에 맞추기 위해 해야 할 필요가 있는 따라잡기 메타 플랫폼 외에도, 한 가지 즉각적이고 골치 아픈 문제가 더 있다(개인 정보 보호 스캔들, 브랜드 악화, 규제 위험, 그리고 필요한 고가의 다년 투자와는 무관하게): 회사의 이해와 함께 본질적으로 깨진 무언가가 있는 것 같다.ng of what is socially permissible and what is not.사회적으로 허용되는 것과 그렇지 않은 것의 ng.According to CPO Magazine, for example, Meta Platforms is any serious gamer will attest.게다가, 앞에서 언급했듯이, 이 회사는 Virtual Reality 헤드셋과 플랫폼에 대한 게임 내 광고를 수익화하려고 시도하고 있는데, 이것은 어떤 심각한 게이머가 증명하듯이 신중하게 하지 않으면 의문스러운 움직임이다.The company is rushed and a tad reckless in its foray into virtual reality.그 회사는 급박하게 가상현실 속으로 빠져들고 있다. It is unclear whether this stems from overconfidence or desperation, yet the warning signs are there for any investor willing to do their due diligence. 이것이 과신에서 비롯된 것인지 아니면 절박함에서 비롯된 것인지는 분명치 않지만, 그들의 실사를 기꺼이 하려는 투자자들에게 경고 신호는 있다. Just days after making Horizon Worlds accessible for all in the USA and Canada, the press circulated coverage about how a woman 있었을 것이다. Furthermore, it clearly demonstrates the incredibly hostile press media Meta Platforms can anticipate in the coming years (as any cunning commentator will observe, the timing of the press releases is suspect). 게다가, 그것은 메타 플랫폼스가 앞으로 몇 년 안에 예상할 수 있는 엄청나게 적대적인 언론 매체들을 분명히 보여준다. (어떤 교활한 평론가들이 관찰하듯이, 보도 자료의 시기는 의심스럽다.)It would be understandable if Meta Platforms focused solely on the Metaverse, yet by announcing the intent to compete in the creator economy, e-commerce, and computing platforms, one gets the sense that the company is overreaching and overextending, needlessly.메타 플랫폼이 메타버스에만 집중했다면 이해할 만하다. 하지만 창조경제, 전자상거래, 컴퓨팅 플랫폼에서 경쟁하겠다는 의도를 발표함으로써, 불필요하게 회사가 과대포장하고 과대포장하고 있다는 느낌을 갖게 된다.Meta Platforms could certainly focus on AR/VR and in building out the necessary infrastructure to facilitate the Metaverse environment, and do so well.메타 플랫폼은 확실히 AR/VR에 초점을 맞추고 메타버스 환경을 용이하게 하기 위해 필요한 인프라를 구축하는 데 초점을 맞출 수 있으며, 그렇게 잘 할 수 있다. By instead expanding the scope of its efforts it risks an increased chance of failure across all projects. 대신 노력의 범위를 확대함으로써 모든 프로젝트에 걸쳐 실패 확률이 증가할 위험이 있다. By announcing the intent to compete in all of these areas, it further draws unwarranted and unnecessary attention from competitors who may have otherwise been taken by surprise. 이 모든 영역에서 경쟁하겠다는 의도를 발표함으로써, 그렇지 않았다면 깜짝 놀랐을지도 모르는 경쟁자들로부터 더 이상 불필요한 관심을 끌어낸다.Simply put, this may be unwise and imprudent.간단히 말해서, 이것은 현명하지 못하고 경솔한 것일 수도 있다.A competitor like Adobe will leverage its existing leadership position as a creative and e-commerce titan to monetize the magic of the Metaverse and of the Web 3.0 far more effectively than any individual social media company or VR / AR company can hope to achieve because it offers world-renowned high-quality software and tools to make dreams a reaAdobe와 같은 경쟁자는 Metavers와 웹 3.0의 마법을 수익화하기 위해 창조적이고 전자 상거래 타이탄으로서의 기존의 리더십 위치를 활용할 것이다. 그것은 꿈을 재창조하기 위한 세계적으로 유명한 고품질 소프트웨어와 도구를 제공하기 때문에 메타버스나 VR/AR 회사가 성취할 수 있는 것보다 훨씬 더 효과적이다.lity.연한Creators will use these tools first and foremost to transition to the Metaverse and to differentiate themselves from the competition, while businesses and merchants will rely upon Adobe's offerings and machine learning / AI capabilities of Adobe Sensei to continue their transition to a digital world.크리에이터들은 이러한 도구를 무엇보다도 먼저 메타버스(Metaverse)로 전환하고 경쟁사와 차별화하기 위해 사용할 것이며, 기업들과 상인들은 디지털 세계로의 전환을 지속하기 위해 Adobe Sensei의 제품 및 머신러닝/AI 기능에 의존하게 될 것이다.

Source: Source: Source: 있으며, 대신 라이선스 계약이나 파트너십을 선택할 수 있다.Yet, as it stands, the two titans seem increasingly poised to clash in the coming decade, and I would not bet against Adobe given its quiet cunning, its strategic leadership in the creator economy, e-commerce, and associated computing platforms, and its exceptional business model and fundamentals.그러나, 현재 상태로는, 두 명의 티격태격자들이 향후 10년 안에 점점 더 충돌할 것 같아 보이고, 나는 Adobe의 조용한 교활함, 창조자 경제, 전자상거래 및 관련 컴퓨팅 플랫폼에서의 전략적인 리더십, 그리고 뛰어난 비즈니스 모델과 펀더멘털을 감안할 때, Adobe와 내기를 걸지 않을 것이다.

>

Source: mbG">

'경제' 카테고리의 다른 글

| 테슬라 주가 전망 :: 미국주식 TSLA (0) | 2021.12.30 |

|---|---|

| 인텔, 대규모 주주 가치 창출에 주력 (0) | 2021.12.29 |

| 2022년 주요 15개 종목 선정 (0) | 2021.12.27 |

| 2030년까지 500달러로 가는 알리바바의 길 (0) | 2021.12.26 |

| AMD Vs. Intel: 내가 AMD에 대해 잘못 알고 있었다. (0) | 2021.12.25 |